First Solar (FSLR) is amongst the world’s largest utility scale solar system installers and producer of solar panels. The company recently released its Q114 results, which showed improvement in revenues, gross margin, shipments, project pipeline etc. FSLR has managed to sharply reduce the cost of its thin film Cadmium Tellurium (Cd-Te) modules, as well as improve its efficiency. Despite the improvement in fundamentals, I still remain negatively biased towards the company. The company has a relatively high valuation and limited growth opportunities, due to its absence in the world’s largest and fastest growing markets of Japan and China. First Solar does not have a presence in rooftop solar segment, unlike the other solar companies such as SunEdison (SUNE) and SunPower (SPWR). It is trying to increase its presence in this segment, but the Cd-Te modules are less efficient than the monocrystalline solar panels made by SunPower. FSLR is trying to enter the silicon panel market after buying Tetrasun, but it has a long way to go before achieving success. SunPower on the other hand, has a strong technology advantage and experience in the rooftop solar panel market.

While First Solar’s fundamentals have improved dramatically, the company’s valuations are pretty high when compared to the other solar stocks and its growth opportunities also seem to be limited. I would advise investors to look at the other solar stocks, whose valuations have declined dramatically in the last few months.

Why First Solar may not be a Buy

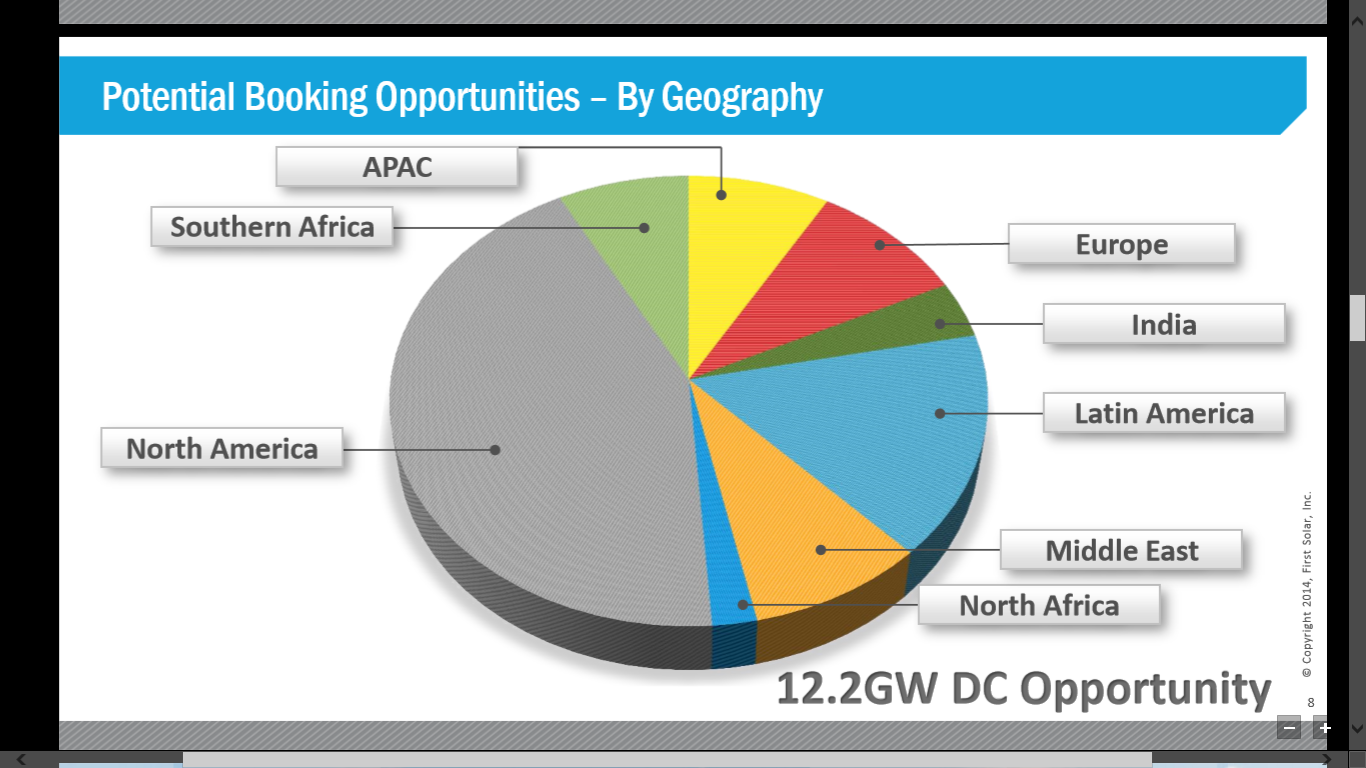

1) Concentrated in North Americas and almost no presence in Japan & China – First Solar is very heavily dependent on the North American utility market for its sales. This sharply limits its growth opportunities. The company has very little presence in Japan and China, which witnessed extremely high solar growth in 2013. Looking at the graph below, we can see that ~ 75% of FSLR’s activity is centered around the Americas, with very little marketshare in Asia and Europe. Though USA is also a good market but First Solar may face the risk of an abrupt decline there, due to a change in policies by the American government (for example expiry of the solar tax credit).

(click to enlarge)

Source: First Solar

2) Transition to Silicon Panel technology will not be easy – First Solar is a world leader of thin film Cd-Te technology, but now the company is also making a foray into silicon solar panels. This will not be easy, as the company will have to manage the sales, R&D, distribution and marketing of two very different technologies. Though the company’s thin film segment has also started performing well, but I think its decision to develop and make its own silicon solar modules might not make sense in today’s cut throat solar industry.

3) Stock Price & EPS volatility – The First Solar stock has varied through peaks and troughs in the last one year. Given below is the graph showing the various stock price points, during the different months. The stock price has recently seen some consolidation and is currently trading at ~$61, which is ~20% below its all-time 52 week high price of $74.8.

(click to enlarge)

Source: Yahoo Finance

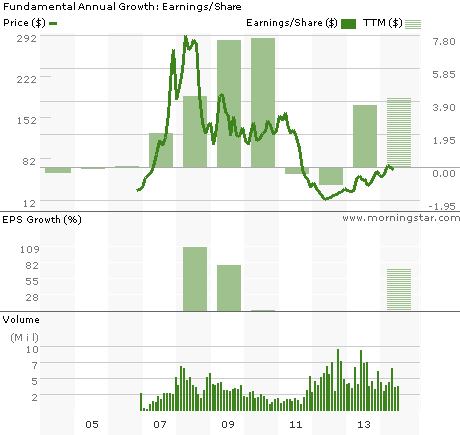

The EPS history of the company is also not very stable. Such a kind of performance brings a level of uncertainty in the minds of the investors.

Source: Morningstar

4) Solar System Business – First Solar is one of the largest solar system developers in the USA and has many projects lined up in the country. However, there is an imminent risk of slowdown in the solar system development business and even USA facing a saturation in such system businesses. There are also two very other strong US solar companies in this line of business – SunPower & SunEdison, giving strong competition to FSLR. Even these companies gave good quarterly results and have a decent project pipeline. I would prefer them to FSLR.

5) First Solar Modules is still not a competitive standalone business – FSLR modules are mostly used in-house by the company for its system business. First Solar used to generate gross margin of greater than 50% during 2008, when the company’s modules used to cost much less than competition. But now companies such as Jinko Solar (JKS) are able to produce solar panel at 50c/watt, which is lower than FSLR’s ~60c/watt cost. The company is not able to sell solar panels in a substantive manner as its ASP is higher and efficiency is lower.

6) Insider Selling – During the first week of May, insiders sold close to 45000 shares of the company. This does not augur well for First Solar, as the stock price is still ~80% below its all-time peak of ~$300.

First Solar Positives

a) Good Q1 2014 results & Annual Guidance – The company gave good first quarter results. Its revenue and gross margin exceeded the guidance given earlier. The revenues rose by ~$200 million to $950 million in Q1 2014, mainly because of the revenue recognition of its Campo Verde project. The EPS was $1.10 in Q1 2014, as compared to $0.64 in Q4 2013. The operating income more than doubled itself from $60 million in Q4 2013 to $139 million in Q1 2014. Total debt decreased by $24 million to $199 million in Q1 2014. The company also gave a robust annual guidance – Net Sales of $4 billion, GM at 17% and EPS at $2.8.

b) Strong Footing in USA – The company is very well established in the USA, with major activities happening in North and Latin Americas (refer to the pie-chart above). There are over 600 MW of new opportunities in the U.S and also an 850 MW AC EPC agreement in California, whose construction begins later this year. There is an EPC agreement for 43 MW AC with the EDF Renewable Energy to build projects on three sides in California, projected to begin this quarter.

Valuation

The stock is not cheap as it will trade at a forward P/E of almost 24x, based on the midpoint of its 2014 EPS guidance. It has a P/S of ~1.5x, which is comparable to the multiples given to the other large US solar stocks such as Sunpower with a forward P/E of ~22x and P/S of 1.9x. I don’t think FSLR is as good as SunPower. Also when compared to the other Chinese solar stocks such as Jinko Solar, FSLR is very expensive. JKS has a forward P/E of just 5x and a P/S of 0.5x.

Summary

First Solar has shown a sharp improvement in its overall business by increasing the efficiency of its thin film modules and reducing costs. The company has also managed to execute well on its North American pipeline by delivering most of its projects on time. However, I find that FSLR’s valuation is a bit high compared to the other solar stocks which have recently become very cheap. High quality Chinese solar stocks such as Canadian Solar (CSIQ), Renesola (SOL), Jinko Solar etc. have shown a 50% decline from their 52 week highs. These stocks have become an absolute bargain and can show sharp returns, as was witnessed during Trina Solar’s (TSL) sharp price jump on Friday, 23rd May. I would look to avoid First Solar to buy other attractive opportunities in the solar market.

Google+